AN INTRODUCTION TO THE SCHEME

Project Report on Soft Drink Manufacturing PMFME

Ministry of Food Processing Industry (MoFPI) has launched the Pradhan Mantri Formalisation of Micro food processing Enterprises (PMFME) scheme under the Aatmanirbhar Bharat Abhiyan with the aim to enhance the competitiveness of existing individual micro-enterprises in the unorganized segment of the food processing industry and promote formalization of the sector. The scheme to be implemented over a period of five years from 2020-21 to 2024-25 with a total outlay of Rupees 10,000 crore.

The Scheme aims to augment the existing individual micro-enterprises in the unorganized segment of the food processing industry and formalize two lakh micro food processing enterprises with special focus on supporting groups such as Farmer Producer Organizations (FPOs), Self-Help Groups (SHGs) engaged in Agri-food processing sector, inter-alia, by providing:

i. Food processing entrepreneurs through credit-linked capital subsidy @35% of the eligible project cost with a maximum ceiling of Rs.10 lakh per unit.

ii. Seed capital @ Rs. 40,000/- per SHG member for working capital and purchase of small tools.

iii. Credit linked grant of 35% for capital investment to FPOs/ SHGs/ producer cooperatives.

iv. Support for marketing & branding to micro-units.

v. Support for common infrastructure and handholding support to SHGs, FPOs and Producer Cooperatives.

vi. Providing Capacity building and training support to increase the capabilities of the enterprises and upgradation of skills of workers.

ABOUT THE PRODUCT:

Carbonated soft drinks constitute the major category in “Aerated Soft Drinks”, the other two categories being juice based soft drinks and squash, sharbat and syrup. Various types of soft drinks including orange, lime and lemon based drinks as well as soda water fall in the category of aerated soft drinks. These water drinks consist of water, carbon-di-oxide, colour, additives and preservative. In a tropical country like India, which has oppressive summers, there is substantial market for aerated soft drinks.

MARKET POTENTIAL:

The all India production of aerated soft drinks is about 900 crore bottles per year, of which the production of carbonated soft drinks is about 70% i.e. 630 crore bottles. The per capita consumption of carbonated drinks is about 4 bottles per year, which is low compared to other developing countries such as Pakistan -13, Bangladesh – 8, Egypt – 3, and extremely low compared to USA where it is 350 bottles. Hence there is considerable potential for consumption to grow. Based on the average per capita consumption of 4 bottles and considering the population of 385 lakhs in the north-eastern region, the demand for aerated water drinks is estimated at 15.40 crore bottles per year. The market is dominated by brands of leading all India companies such as Parle (46%), Pure Drinks (23%), McDowel (7%). Every State has its own local brands which have their own market. There are one or two local brands, which have alimited production. Assuming that local units can get 5% of the market, i.e. 77 lakh bottles and considering the capacity of typical tiny unit of about 15 lakh bottles per year. there appears to be scope for 2 or 3 units to be set up.

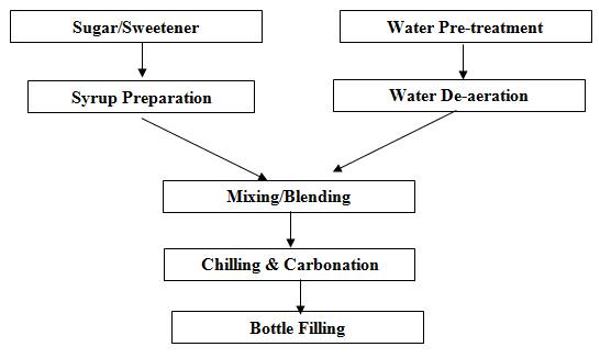

MANUFACTURING PROCESS:

The main process steps are:

i) Making concentrate of sugar, glucose, citric acid, essence and preservatives.

ii) Feeding the concentrate into dosing machine.

iii) Releasing the concentrate in each bottle in a required proportion.

iv) Filling the bottle with treated water.

v) Placing crown-cork on the bottle and passing through a shaker for proper mixing.

BASIS AND PRESUMPTIONS:

a) This Report is worked out the basis of 75% capacity utilization on single shift and 300 working days per annum. b) The machinery and equipment are of standard make. c) The cost of raw materials and other expenditure is approximate and based on current market rates. d) The period for achieving capacity utilization is estimated to be one year after commencement of production.

POLLUTION CONTROL:

The process of manufacture does not generate pollution. However, entrepreneurs are to contact State Pollution Control Board for necessary guidance.

ENERGY CONSERVATION:

Maximum care should be taken while selecting the machinery and other electrical equipment so as to ensure minimum power consumption.

CONSTITUTION OF THE UNIT:

The proposed unit will be set up as a proprietorship concern of whose bio-data has been mentioned in the first chapter of this project report.

In the proposed enterprise, the promoter will be personally involved in the day-to- day operation. He will not only supervise marketing, dispatch, collection and other related activities of the unit but will also putting his own expertise in all these tasks.

The proprietor is honest, dependable and laborious. He is energetic and quite fit for bring in big success to the unit.

LOCATION AND IT'S ADVANTAGES:

The proposed unit will be set up at the following location in name & style of M/S ........................................................:

.........................add your address of unit here..................................

This unit is RENTED/ Owned by the proprietor with some construction on it. The site is very suitable for the proposed unit and concerned skilled worker and helpers are also available,

CAPITAL COST ESTIMATES:

The capital cost of the project consists of the cost includes incurred against the procurement of machineries etc. and pre-operative expenses. The total capital costs is to be incurred have been worked out to Rs. 34,81,000/-

Following are the particulars of the cost of Project:

| S. NO. | PARTICULARS | PRICE |

| 1. | Land | Rented/ Owned |

| 2. | Work Shed/ Building | Rented/ Owned |

| 3. | Plant & Machinery | 34,81,000 |

| Total | 34,81,000.00 | |

ABOUT THE PLANT & MACHINERY:

The Plant & Machine proposed for the knitting & Garment Industry are as follows:

· Automatic Soda Filling machine;

· Carbonation System For Co2 Mixing;

· Shrink Tunnel For Manual Labeling;

· Automatic Shrink Wrapping Machine;

· Mixing Tank & Filter Press With PHE;

OPERATING COST ESTIMATES:

In computing the cost under this head, all expenses including the cost of raw materials, manpower, power and fuel have duly been considered.

RAW MATERIAL

Main Raw Materials are:

- Sugar

- Citric Acid

- Essence

- Activated Carbon

- Caustic Soda

- Liquid Glucose

- Carbon-di-oxide

These raw material are available in local market or delhi. The estimated cost for 1 operating cycle is Rs. 8 lacs

POWER & FUEL:

Electricity power requirement is for General Use for using equipment & for lightening and fan in the shop. Also some of the Machinery will require some amount of Power. Most of the power requirements will be fulfilled by the Government Electricity.

MANPOWER & MANAGING COST:

The overall management and sales supervision will be done by the proprietor. The requirement of manpower and managing cost has been estimated as under:

| S. No. | Types of Manpower | Strength | Wages | Monthly Salary (Rs.) | AnnualSalary (Rs.) |

| 1. | Skilled | 5 | 9,000 | 45,000 | 5,40,000 |

| 2. | Unskilled Workers | 20 | 7,000 | 1,40,000 | 16,80,000 |

| TOTAL | 25 | 1,85,000/- | 22,20,000 | ||

* As per the Minimum Wages Guidelines by applicable states.

OTHER EXPENSES:

Other Expenses would include Repair & Maintenance, Postage & Stationery, Insurance, Transportation etc. This would cost approximately about 1,00,000 per Annum.

SELLING EXPENSES:

Selling Expenses has been considered @ 5% of sales volume to meet the expenses on account of sales incentives and sales promotion expenses.

FINANCIAL IMPLICATIONS:

The cost to the project has been estimated as Rs. 45,00,000/-, which includes the capital cost of Rs. 34,81,000/- and for working capital as Rs. 10,19,000/-.

The rates of interest for the term loan and working capital loan have been taken as 12% per year respectively for the purpose of forecasting the profitability of the venture. Depreciation has been considered at 15% on Plant & Machinery.

Selling price of the finished goods & services taken, are competitive in the prevailing market. The whole working results are shown in the projected performance and profitability statement. The pay back period of the term loan has been taken in Five years.

The working capital loan has been proposed to be repaid in Five Years. The B.E.P. analysis is shown in Break-even point analysis according to which the project at 50% capacity utilities would break even at 81.39%.

These values and analysis as referred above and in the four pages are reasonable and realization. Thus, On the basis of the foregoing analysis, it is concluded that the unit’s proposal is technically feasible and economically viable and therefore, the project is recommended for implementation under the PMFME Scheme.

Project Report on Soft Drink Manufacturing PMFME

Apart from these details you need to make cover page, Project Summary, Financial Reports. Link on the below link for free download the all three files.

Read more: Project Report on Soft Drink Manufacturing PMFME